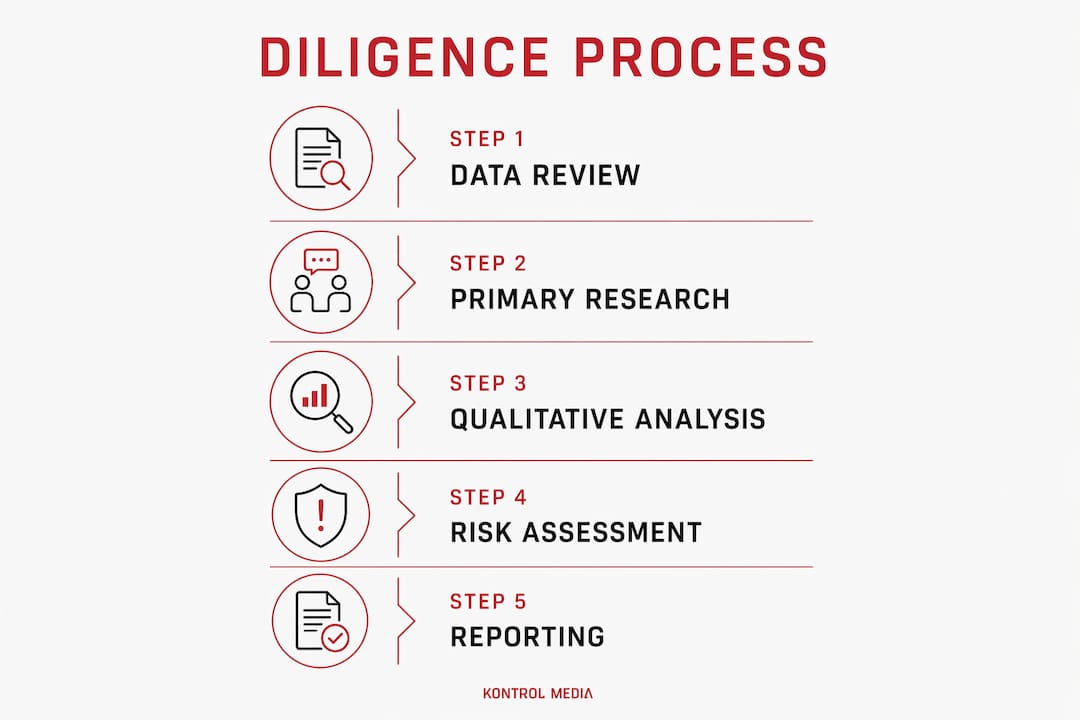

Private equity marketing due diligence is the rigorous assessment of a target company’s marketing unit economics, channel mix, and operational maturity to verify scalable and sustainable growth potential before investment. This process sits at the intersection of financial underwriting and commercial strategy, and it has become a non-negotiable step in competitive deal processes. The core question every PE team must answer is whether the company can acquire customers profitably and sustain that acquisition at scale. Metrics like Customer Acquisition Cost (CAC), Lifetime Value (LTV), and the CAC:LTV ratio are the primary instruments for that answer. Getting this wrong does not just affect valuation. It shapes the entire post-close growth thesis.

What does private equity marketing due diligence actually measure?

The foundation of any marketing diligence process is unit economics. CAC and LTV are the two metrics that determine whether a company’s growth is genuinely profitable or just expensive revenue. CAC measures the total cost to acquire one customer, and LTV measures the total revenue that customer generates over their relationship with the business. The ratio between them tells you whether the business model is structurally sound.

One of the most common mistakes in the marketing diligence process is an incomplete CAC calculation. A comprehensive CAC calculation must include media spend, creative development, personnel costs, and technology fees, not just ad spend. Companies that report only paid media in their CAC figures can appear far more efficient than they actually are. This creates a misleading picture of growth economics that surfaces painfully after close.

PE teams apply specific benchmarks when evaluating these ratios. A CAC:LTV ratio of 3:1 is the minimum threshold for a healthy business, with ratios of 4:1 or higher signaling strong scalability. Ratios below 3:1 are a red flag, suggesting the business is spending too much to acquire customers relative to the value those customers generate. Payback period is equally telling. Targets with payback periods under 12 months are preferred, since longer payback windows increase capital exposure and reduce flexibility post-acquisition.

Channel concentration is another quantitative risk factor that gets underweighted in early screening. A company generating more than 60% of its customer acquisition from a single channel, whether that is Google Ads, Meta, or a single affiliate partner, carries meaningful concentration risk. If that channel degrades, costs rise, or the platform changes its algorithm, the entire acquisition engine is exposed. Unit economics like payback period and pipeline coverage are the real indicators of cash efficiency, not follower counts or engagement rates.

Pro Tip: When modeling CAC at scale, test the efficient frontier by projecting how CAC and payback period change if marketing spend doubles post-close. Some businesses show excellent unit economics at current spend levels but deteriorate sharply as budgets increase, which is a critical signal for underwriting post-acquisition growth plans.

| Metric | Benchmark |

|---|---|

| CAC:LTV ratio | 3:1 minimum; 4:1+ preferred for scalable growth |

| Payback period | Under 12 months preferred; over 18 months is a concern |

| Channel concentration | No single channel above 60% of acquisition volume |

| LTV cohort analysis | Cohort retention should be stable or improving over time |

What qualitative factors matter beyond the numbers?

Quantitative metrics tell you what is happening. Qualitative assessment tells you why, and whether it can be replicated. The marketing team’s depth and structure is one of the first things to evaluate. Key-person risk is a real concern when a single CMO or growth lead owns all channel relationships, agency contracts, and institutional knowledge. If that person leaves post-close, the marketing function can stall for months.

Documentation maturity is a reliable proxy for operational readiness. Companies with well-documented standard operating procedures (SOPs), brand guidelines, and channel playbooks are far easier to scale than those running on tribal knowledge. Contracts with agencies and technology vendors should be reviewed for ownership clauses, particularly around creative assets and first-party data. Data ownership issues discovered post-close are expensive to resolve.

The martech stack deserves its own assessment. Vendor lock-in, disconnected data silos, and attribution gaps are common in companies that have grown quickly without a deliberate technology strategy. A company running five separate analytics tools with no unified attribution model cannot give you a reliable read on which channels are actually driving revenue. Marketing diligence ultimately underwrites cash efficiency and revenue conversion, and that requires clean, trustworthy data.

Audience asset ownership is a factor that often gets overlooked. A company with a large, engaged email list or a substantial first-party data asset has a durable acquisition advantage that does not depend on paid media costs. Contrast that with a business whose entire audience lives on rented platforms. The former is a genuine asset; the latter is a recurring liability.

Pro Tip: Ask the company to walk you through their attribution model in detail. If they cannot clearly explain how they assign credit across channels, or if their attribution relies entirely on last-click, the reported CAC figures are likely understating true acquisition costs.

Here are the qualitative factors that carry the most weight in a thorough investor marketing analysis:

- Marketing team structure, depth, and key-person dependencies

- Documentation maturity: SOPs, brand guidelines, and channel playbooks

- Martech stack coherence and attribution accuracy

- First-party data ownership and audience asset quality

- Agency and vendor contract terms, particularly data and creative ownership clauses

- Organic traffic trends and content asset sustainability

Why does primary research change the outcome of diligence?

The Confidential Information Memorandum (CIM) is a starting point, not a source of truth. Management teams present their best narrative in a CIM, and that narrative is almost always optimistic. Treat the CIM as a baseline and then validate every material claim by mapping it to tracking data, CRM records, and cohort analysis within the data room. The gap between what the CIM says and what the data shows is often where the real deal risk lives.

Proprietary primary research is the mechanism for closing that gap. Customer calls, B2B surveys, competitor interviews, and channel checks provide independent validation that no data room document can replicate. When customers describe why they chose the company, how they found it, and whether they would renew, you get a ground-level view of the acquisition and retention story that management cannot script.

The timing of primary research matters as much as the method. Pre-LOI screening calls with two or three customers can sharpen your deal thesis before you commit significant resources. Post-LOI confirmatory diligence goes deeper, with structured surveys across a statistically meaningful customer sample and direct competitor checks to validate market positioning claims. Rigorous commercial diligence relies on this triangulation to ground-truth management narratives and provide a decisional edge over competing bidders.

Here is a practical sequence for structuring primary research across the deal process:

- Pre-LOI: Conduct two to four customer discovery calls to test the core value proposition and acquisition story.

- Pre-LOI: Run a quick competitor check with two or three channel partners or distributors to validate market share claims.

- Post-LOI: Deploy a structured customer survey across 20 to 50 accounts to quantify satisfaction, retention drivers, and switching risk.

- Post-LOI: Conduct expert calls with former employees or industry practitioners to assess team quality and operational claims.

- Post-LOI: Triangulate all primary findings against CRM data, attribution reports, and cohort analyses in the data room.

“The most valuable insight from primary research is rarely what customers say about the product. It is what they reveal about how they found it, why they stayed, and what would make them leave. That is the real marketing story.”

The market research process that supports commercial diligence is not a checkbox exercise. It is the mechanism that separates a confident investment thesis from an expensive assumption.

What does the diligence timeline look like, and what are the red flags?

Marketing diligence typically spans 3 to 8 weeks within the broader PE process, with ideal preparation starting 12 to 18 months before a transaction. Companies that begin preparing early can remediate issues, improve documentation, and build a credible marketing narrative rather than scrambling to explain gaps under deal pressure.

The documentation package PE teams expect includes marketing spend reports broken out by channel and cohort, CAC analyses with full cost components, org charts with tenure and reporting lines, SOPs for key marketing functions, agency and vendor contracts, and compliance records for regulated channels. Missing or inconsistent documentation is itself a signal, not just an inconvenience.

The red flags that most frequently affect valuation or deal viability fall into two categories: economic and operational.

| Red Flag | Potential Impact |

|---|---|

| Rising CAC without explanation | Signals deteriorating channel efficiency or increased competition |

| Channel concentration above 60% | Creates single-point-of-failure risk for acquisition volume |

| Undocumented processes and missing SOPs | Increases key-person risk and post-close integration cost |

| Declining organic traffic trends | Suggests weakening brand authority and rising paid dependency |

| Data ownership gaps in vendor contracts | Creates legal and operational risk around first-party assets |

| CAC:LTV ratio below 3:1 | Indicates structurally unprofitable customer acquisition |

Valuation adjustments tied to marketing red flags are increasingly common. A company with a 60% channel concentration in paid search and a rising CAC trend may still be a viable investment, but the risk premium is real and the post-close value creation plan needs to address it directly. Early preparation gives sellers the time to fix what is fixable and frame what is not.

Key takeaways

Effective private equity marketing due diligence requires validated unit economics, diversified channel infrastructure, and primary research to confirm that growth is both profitable and repeatable at scale.

| Point | Details |

|---|---|

| CAC must be fully loaded | Include media, creative, personnel, and technology costs to avoid understating true acquisition expense. |

| CAC:LTV ratio sets the floor | A ratio below 3:1 signals structural risk; 4:1 or higher supports scalable growth underwriting. |

| Primary research validates the CIM | Customer calls and competitor checks reveal risks that data room documents cannot surface. |

| Channel concentration is a deal risk | Any single channel above 60% of acquisition volume creates fragility in the growth model. |

| Preparation starts 12 to 18 months early | Early remediation of documentation and process gaps produces a materially stronger diligence outcome. |

What I have learned from doing this work in the field

I have sat across the table from management teams presenting polished CIMs with impressive CAC figures, and I have also been the person asking the uncomfortable follow-up questions. The gap between what gets presented and what the data actually shows is rarely malicious. It is usually the result of teams measuring what is easy rather than what is complete.

The single biggest mistake I see PE teams make is treating marketing diligence as a documentation review rather than a stress test. You can collect every report in the data room and still miss the fact that the company’s CAC doubles when spend increases by 50%. Modeling scalable CAC scenarios is not optional. It is the difference between underwriting a real growth plan and inheriting a problem.

I also believe primary research is chronically underused in marketing diligence, particularly at the pre-LOI stage. Most teams wait until post-LOI to talk to customers, which means they have already committed significant resources before testing the core acquisition story. Two or three customer calls before the LOI can reshape the entire deal thesis, and they cost almost nothing relative to the risk they reduce.

The qualitative work matters just as much as the numbers. A marketing team with deep channel expertise, clean documentation, and owned audience assets is a genuine value creation lever. A team built around one person with no playbooks and agency-controlled data is a liability, regardless of what the topline growth chart shows. I have seen both, and the operational texture of the marketing function is one of the clearest signals of what post-close integration will actually look like.

The firms that get this right start early, go deep on primary research, and integrate their marketing diligence findings directly into the 100-day plan. That is not a best practice. It is the standard.

— Mark Kapczynski

How Kontrol Media supports your marketing diligence process

Kontrol Media works directly with private equity teams and portfolio companies to bring rigor and clarity to the marketing diligence process. From building out fully loaded CAC analyses to conducting primary customer and competitor research, the work is hands-on and built around the specific deal context, not a generic framework.

For firms that need to validate growth assumptions, assess marketing infrastructure, or build a post-close marketing plan grounded in real data, Kontrol Media’s marketing ROI analysis service provides the analytical depth that deal teams require. The team has worked with organizations including Experian, West Monroe, and REMAX, and brings that same performance-focused methodology to PE-backed companies at every stage of the investment cycle. If you are preparing for a transaction or working through a current diligence process, explore Kontrol Media’s marketing strategy services to see how the work gets done.

FAQ

What is private equity marketing due diligence?

Private equity marketing due diligence is the systematic evaluation of a target company’s marketing unit economics, channel mix, team capabilities, and data infrastructure to assess whether growth is profitable and scalable. It focuses on metrics like CAC, LTV, and payback period rather than vanity metrics like impressions or follower counts.

What CAC:LTV ratio do PE investors look for?

PE investors treat a 3:1 CAC:LTV ratio as the minimum acceptable benchmark, with 4:1 or higher preferred for companies being underwritten on a growth thesis. Ratios below 3:1 typically trigger valuation adjustments or require a clear remediation plan.

How long does marketing due diligence take?

The marketing diligence process typically spans 3 to 8 weeks within the broader PE deal timeline. Companies that begin preparing 12 to 18 months before a transaction are in a significantly stronger position to present clean data and address potential red flags proactively.

Why is primary research important in marketing diligence?

Primary research, including customer calls, competitor checks, and structured surveys, validates the claims made in the CIM against independent sources. It surfaces risks and value creation opportunities that internal data and management presentations routinely obscure.

What are the most common marketing due diligence red flags?

The most common red flags include rising CAC without a clear explanation, channel concentration above 60% in a single acquisition source, undocumented marketing processes, declining organic traffic, and data ownership gaps in agency or vendor contracts. Each of these can affect both valuation and post-close integration complexity.

Recommended

- Private Equity Commercial Due Diligence: 2026 Guide | Kontrol Media Consultancy

- Unlocking Business Potential: Strategic Marketing and Consulting for Growth | Kontrol Media Consultancy

- What Is Marketing-Led Growth? A Strategic Guide | Kontrol Media Consultancy

- Growth Through Acquisition Marketing Explained for Leaders | Kontrol Media Consultancy