Private equity commercial due diligence is defined as a forward-looking, systematic assessment of a target company’s market environment, competitive position, customer dynamics, and growth potential, conducted to validate the investment thesis before capital is committed. Unlike financial due diligence, which interrogates historical performance, or legal diligence, which maps liability exposure, commercial due diligence asks the harder question: does this market actually support the returns we are projecting? Frameworks from Carta and Woozle’s 2026 practitioner guide both treat it as a distinct discipline, one that separates market story from market reality through primary research, expert calls, and B2B surveys. Getting it right is the difference between a thesis that holds and one that quietly unravels eighteen months post-close.

What are the core components of the commercial due diligence process?

Commercial due diligence is a systematic, forward-looking assessment that tests the investment thesis against competitive position, growth potential, and customer dynamics. Each component maps directly to an assumption in your financial model, which is why skipping any one of them creates a blind spot that shows up later in portfolio performance.

The five core components every deal team should work through are:

Market sizing and growth drivers. This means quantifying the total addressable market, the serviceable addressable market, and the realistic share the target can capture. Growth drivers include structural trends like regulatory shifts, demographic changes, or technology adoption curves. A market that looks large on paper but is growing at 2% annually with heavy commoditization tells a very different story than one expanding at 15% with fragmented supply.

Competitive landscape and positioning. You need to understand where the target sits relative to direct competitors, adjacent players, and potential new entrants. Switching costs are a critical signal here. High switching costs indicate durable competitive position; low switching costs mean customer retention is always one bad quarter away from becoming a churn problem.

Customer dynamics and concentration risk. Customer base stability is one of the most scrutinized elements in any private equity investment analysis. If the top three customers represent 60% of revenue, that concentration risk belongs in your valuation model, not just your risk register. Churn rates, net promoter scores, and contract renewal patterns all feed into this assessment.

Growth potential and scalability. This covers new market entry, product line expansion, geographic expansion, and whether the operational infrastructure can scale without proportional cost increases. A company with strong unit economics in one region may face entirely different dynamics when it tries to replicate that model nationally.

Thesis alignment. Every finding from the four components above should map back to the specific assumptions underpinning your investment thesis. If your thesis assumes 20% annual revenue growth driven by market expansion, your commercial diligence needs to either confirm that the market supports it or flag where the assumption breaks down.

How is primary research conducted during commercial due diligence?

Primary research is the engine of credible commercial diligence. Secondary data, industry reports, and management presentations give you the story. Primary research tells you whether the story is true. Rigorous primary research separates investment-grade evidence from polished narrative by verifying management claims through direct conversations with customers, competitors, and suppliers.

Here is how a well-structured primary research program runs in practice:

Expert calls, pre-LOI phase. Before the letter of intent is signed, run three to five expert calls with former executives, industry operators, or sector specialists. The goal at this stage is thesis sharpening, not confirmation. You want to identify the questions that matter most before you commit to a full diligence budget.

Expert calls, post-LOI phase. After the LOI, scale to 8 to 15 expert calls targeting a mix of former company insiders, competitor executives, channel partners, and end-market specialists. Effective interview planning sequences sourcing before call waves, runs mid-program synthesis to adjust the discussion guide, and uses follow-up calls to close gaps before the investment committee presentation.

B2B customer surveys. A well-designed B2B survey with 30 to 100 or more respondents gives you statistical validation of customer satisfaction, churn risk, and willingness to pay. This is not a qualitative exercise. The data should be granular enough to support segment-level analysis and feed directly into your financial model scenarios.

Channel checks. Conversations with distributors, resellers, and implementation partners surface ground-level intelligence that customers and management will not volunteer. Channel partners often have the clearest view of competitive dynamics, pricing pressure, and where the target is winning or losing deals.

Independent customer recruitment. Never let the seller control who you talk to. Seller-facilitated recruitment systematically excludes at-risk or dissatisfied customers, which is one of the most common ways commercial diligence misleads investors. Independent recruitment through third-party panels or direct outreach produces a representative sample.

Pro Tip: Start your B2B survey design in parallel with expert call sourcing, not after. Survey design informed by early expert call themes produces sharper questions and more actionable data, and it protects you when the timeline compresses.

What is the typical timeline and phased workflow for commercial due diligence?

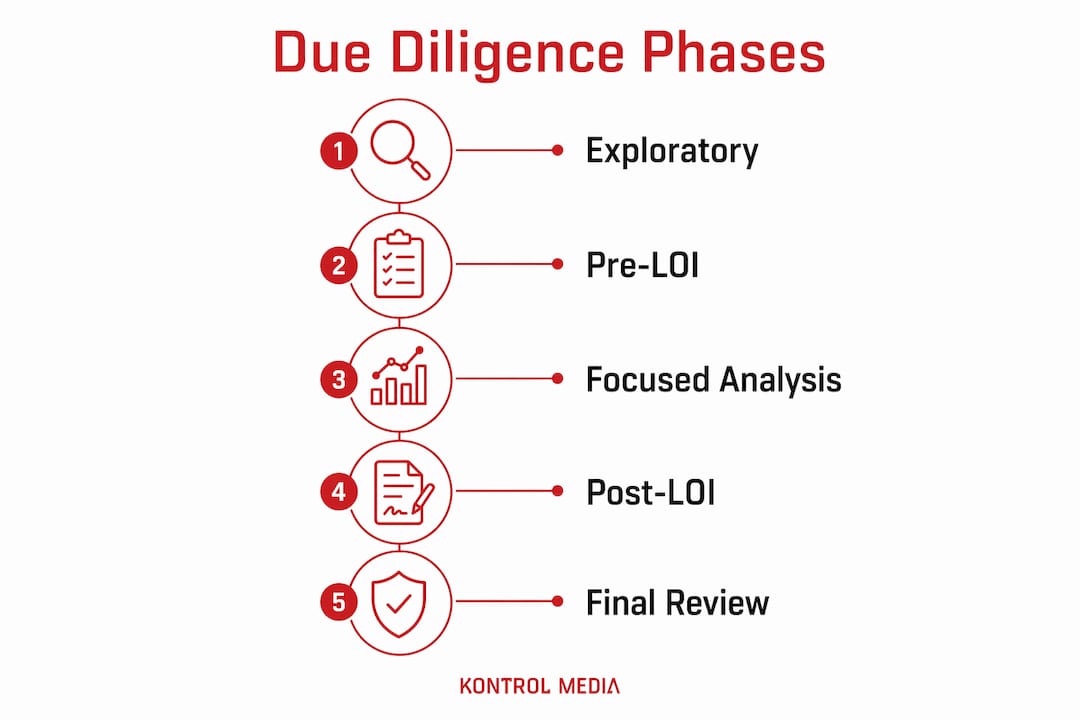

The commercial due diligence process fits into a two-phase structure that mirrors the broader deal timeline. Understanding where each phase begins and ends helps you allocate research budget efficiently and avoid the common mistake of front-loading secondary analysis when primary research is what actually moves the needle.

| Phase | Timing | Primary Activities | Key Output |

|---|---|---|---|

| Exploratory diligence | Pre-LOI | 3 to 5 expert calls, market sizing, thesis development | Early risk identification, go or no-go signal |

| Confirmatory diligence | Post-LOI | 8 to 15 expert calls, B2B survey, channel checks, competitive mapping | Thesis validation, IC materials, value creation plan |

| Survey execution | Within post-LOI window | B2B survey fielding and analysis | Customer satisfaction, churn risk, willingness to pay data |

| Synthesis and delivery | Final 3 to 5 days | Cross-source triangulation, scenario modeling, deliverable preparation | Investment committee presentation, post-close handoff |

CDD projects typically run 2 to 8 weeks, and B2B survey execution alone takes approximately 10 to 14 days. That means in a compressed four-week deal, the survey needs to launch on day one, not after the data room opens. Waiting for question finalization or data room access before starting survey work is one of the most avoidable timeline failures in the field.

A thesis-driven approach starting pre-LOI increases efficiency and reduces wasted confirmatory diligence budget by ensuring every research activity maps to a specific investment thesis assumption. Teams that start primary research at the screening stage arrive at the post-LOI phase with sharper hypotheses and clearer kill criteria, which makes the confirmatory phase faster and more decisive.

How do commercial due diligence findings impact valuation and post-acquisition strategy?

Commercial diligence findings are not a narrative appendix to the financial model. They are inputs that directly shape base, upside, and downside scenarios. CDD outputs update financial model scenarios and inform risk assessment and value creation plans in ways that go well beyond qualitative conclusions.

The most direct connection between commercial findings and valuation runs through these risk factors:

Customer concentration. Identifying that a single customer represents 30% or more of revenue is not just a risk flag. It is a valuation input. Customer concentration risks directly affect deal pricing and post-acquisition portfolio strategy, often justifying a lower entry multiple or a structured earnout tied to customer retention milestones.

Churn risk and recurring revenue quality. If your B2B survey reveals that 25% of customers are actively evaluating alternatives, the recurring revenue assumption in your model needs to be stress-tested. That finding changes your base case and almost certainly changes your price.

Competitive threats and market share trajectory. A target that holds 18% market share in a consolidating market looks very different from one holding 18% in a market where a well-funded competitor is taking share quarter over quarter. The trajectory matters as much as the current position.

Value creation hypotheses. Commercial diligence does not just identify risks. It surfaces the specific growth levers that inform your 100-day plan and three-year value creation roadmap. If channel checks reveal that the target is underrepresented in a high-growth vertical, that becomes a priority for the operating team from day one.

Leading PE firms treat commercial due diligence not as a pre-close checkbox but as the foundation for value creation starting Day 1 post-acquisition. The deal teams that get the most out of their diligence are the ones who hand off a commercial intelligence brief to the portfolio operations team the moment the deal closes, not six months later.

What are common pitfalls and best practices in executing commercial due diligence?

The most expensive mistakes in commercial diligence are not analytical failures. They are process failures. Teams that run rigorous analysis on the wrong sample, or synthesize too little data too late, produce deliverables that look thorough but miss the signals that matter.

The most consequential pitfall is selection bias in customer interviews. Seller-facilitated recruitment excludes at-risk or unhappy customers and produces a systematically optimistic picture of customer satisfaction and retention. Independent recruitment through third-party panels or direct outreach is the only reliable mitigation. This is not a minor methodological preference. It is the difference between investment-grade insight and a curated reference list.

Sample size is the second failure mode. At least 50 independent interviews are required to produce statistically robust signals and support segment-level analysis. Teams that rely on 10 to 15 customer conversations are building conviction on outliers, and outliers in either direction will mislead you. The minimum is 50. More is better when the deal size justifies it.

Pro Tip: Design your research around testable hypotheses and explicit kill criteria before a single call is scheduled. If you cannot articulate what finding would cause you to walk away from the deal, your research design is not thesis-driven. It is confirmation-seeking.

“Triangulation across management claims, customers, competitors, and data is essential to building conviction and identifying divergences that need further investigation.” — Woozle Research, Primary Research for Commercial Due Diligence

The best commercial diligence deliverables synthesize across all data sources rather than presenting each stream in isolation. A customer survey finding that contradicts a management claim is only useful if the synthesis layer connects those two data points and draws a conclusion. Data dumping, presenting raw findings without interpretation, is the most common reason a technically thorough diligence process still fails to inform the investment decision.

You can also strengthen your market research approach by building triangulation into the research design from the start, not as an afterthought during synthesis.

Key takeaways

Effective private equity commercial due diligence requires thesis-driven primary research, independent customer recruitment, and direct integration of findings into financial model scenarios and post-close value creation plans.

| Point | Details |

|---|---|

| Start primary research pre-LOI | Run 3 to 5 expert calls before the LOI to sharpen the thesis and reduce wasted confirmatory budget. |

| Use independent customer recruitment | Seller-facilitated recruitment creates selection bias; independent sourcing produces reliable, representative insight. |

| Require minimum 50 interviews | Fewer than 50 customer interviews cannot support segment-level analysis or statistically robust conclusions. |

| Connect findings to financial models | CDD outputs should update base, upside, and downside scenarios, not just inform a narrative risk section. |

| Treat CDD as a Day 1 asset | Hand off commercial intelligence to the portfolio operations team at close to accelerate value creation from the start. |

What I’ve learned about commercial diligence after watching deals go wrong

I have seen deals where the financial model was airtight and the legal review was spotless, but the commercial diligence was thin. Three expert calls, a handful of customer references the seller provided, and a market sizing exercise pulled from a third-party report. The investment committee approved the deal. Eighteen months later, the team discovered that two of the target’s top three customers were already in conversations with a competitor, and the market growth rate the model assumed was based on a segment the company did not actually serve.

That pattern repeats more often than anyone in the industry likes to admit. Commercial diligence is chronically underinvested relative to financial and legal review, partly because its outputs are harder to audit and partly because deal timelines create pressure to compress the work that feels most qualitative. That is exactly backwards. The market and customer reality is what determines whether the financial model ever comes true.

What I have found actually works is treating the commercial diligence brief as a living document that starts at screening and gets handed to the operating team at close. The firms that do this consistently make better entry decisions and build value faster post-acquisition because they are not rediscovering the market from scratch after the deal is done. You can explore how business development opportunities connect to commercial intelligence for a sharper view of how this plays out in practice.

The uncomfortable truth is that most deal teams know what rigorous commercial diligence looks like. They just do not always have the time, the process, or the external support to execute it at the level the deal deserves.

— Mark Kapczynski

How Kontrol Media supports private equity firms with market and customer insights

Kontrol Media works with private equity firms and their portfolio companies to build the kind of market and customer intelligence that commercial diligence demands. That means market opportunity analysis, competitive positioning assessments, and customer satisfaction measurement designed to produce investment-grade findings, not polished presentations with thin data underneath.

If you are evaluating a target and need a sharper read on market size, growth trajectory, or customer retention risk, Kontrol Media brings the research rigor and strategic context to make those findings actionable. Our work with clients like Experian, West Monroe, and Enthusiast Gaming reflects a methodology built around strategic marketing and consulting for growth that translates directly into value creation for PE-backed businesses. Reach out to discuss how we can support your next deal.

FAQ

What is commercial due diligence in private equity?

Commercial due diligence is a forward-looking assessment of a target company’s market environment, competitive position, customer dynamics, and growth potential, conducted to validate the investment thesis before acquisition. It differs from financial due diligence by focusing on future market realities rather than historical performance.

How long does a commercial due diligence project take?

Commercial due diligence projects typically run 2 to 8 weeks, with B2B survey execution alone requiring approximately 10 to 14 days. Compressed timelines require survey work to begin immediately rather than waiting for data room access.

How many expert calls are needed for commercial due diligence?

A practical research plan includes 3 to 5 expert calls pre-LOI for initial thesis validation and 8 to 15 expert calls post-LOI for confirmatory research, targeting former insiders, competitor executives, and channel partners.

Why does independent customer recruitment matter in commercial diligence?

Seller-facilitated recruitment systematically excludes dissatisfied or at-risk customers, producing a misleading picture of retention and satisfaction. Independent recruitment through third-party panels or direct outreach is the only way to generate a representative customer sample.

How do commercial due diligence findings affect deal valuation?

CDD findings directly update financial model scenarios by quantifying risks like customer concentration, churn probability, and competitive threats, which in turn affect entry multiples, deal structure, and earnout terms.

Recommended

- Identifying and Capitalizing on Business Development Opportunities | Kontrol Media Consultancy

- Conducting a Comprehensive Analysis: A Guide to Informed Decision-Making | Kontrol Media Consultancy

- Unlocking Business Potential: Strategic Marketing and Consulting for Growth | Kontrol Media Consultancy

- Navigating Uncertainty: Creating a Resilient Business Strategy | Kontrol Media Consultancy